InP Substrates for Semiconductor Lasers: The Critical Backbone Powering AI Data Centers in 2026

- David Rogers

- AI Buildout Supply Chain

- 2026-07-13

In the shadow of AI’s relentless scaling, one material determines the future of how fast GPUs can actually talk to each other: Indium Phosphide (InP) substrates. Unlike silicon (indirect bandgap), InP’s direct bandgap enables highly efficient conversion of electricity into coherent laser light precisely at the telecom windows (1.3–1.55 μm) where optical fiber loss is minimal /Optica/. This makes it the foundational platform for high-performance semiconductor lasers: distributed feedback (DFB), electro-absorption modulated, and tunable lasers along with full monolithic photonic integrated circuits (PICs) that integrate lasers, semiconductor optical amplifiers (SOAs), modulators, and photodetectors on a single chip.

While modern datacenter transceivers utilize a mix of platforms including GaAs-based VCSELs for short-reach links /EI/ and Silicon Photonics (SiPh) for complex optical engines, virtually every single-mode high-speed transceiver relies on an InP (Indium Phosphide) laser source to generate the primary optical carrier wave. As hyperscalers rapidly transition to 800G and 1.6T architectures, demand for high-speed InP laser dies is surging; the shift to parallel optical lanes (such as moving from 4-channel 400G to 8-channel 800G/1.6T) effectively doubles the discrete laser die count required per transceiver module /IEEE/.

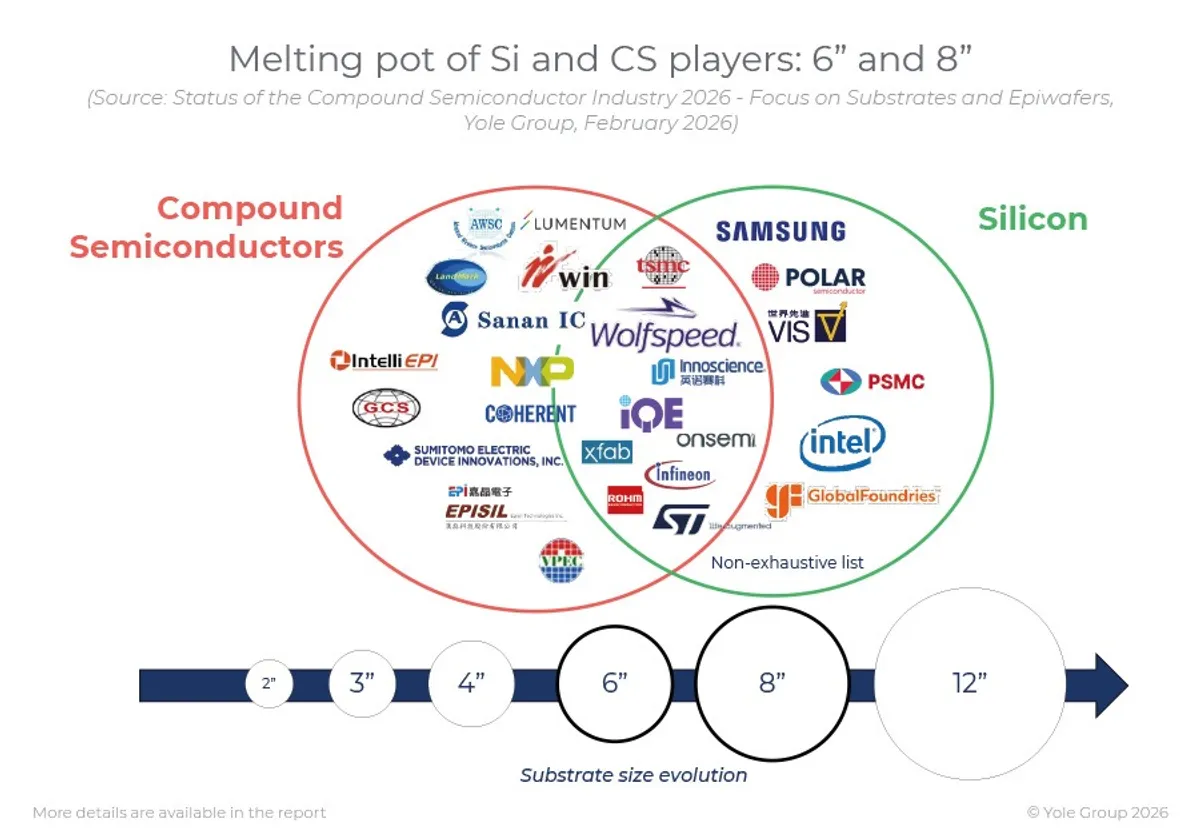

Yet 2026 has brought a stark reality: severe InP substrate shortages /Yole/. Supply is highly concentrated (top players like Sumitomo Electric, AXT, and JX Advanced Metals dominate), lead times are long, and geopolitical export controls have tightened availability. Prices have climbed sharply, and new capacity takes years to qualify and ramp.

Alternative compound semiconductor engineered substrates such as thin InP layers on larger, lower-cost GaAs wafers (InP-on-GaAs) are delivering comparable device performance with dramatically lower cost potential (up to 80% savings at scale) and better scalability to 6-inch+ formats. Fraunhofer ISE and partners have already demonstrated InP-on-GaAs or kerfless epitaxial silicon (EpiWafers) wafers with excellent uniformity and low defect densities /AIP/. Major suppliers are also investing aggressively as JX Advanced Metals alone committed up to ¥120 billion (~$800M) over four years to expand capacity 7-10× specifically for AI-driven optical communications demand /JX/.

Despite these challenges and promising alternatives, Indium Phosphide continues to underpin the optical interconnects essential for AI scaling /NVIDIA/. Continued investment in both traditional substrate capacity and engineered solutions will be critical to meeting the explosive demand for high-speed lasers. The race to secure reliable InP supply may well define the pace of next-generation data center deployments through the end of the decade.

Key Insights

Why can’t copper handle interconnects when 576 GPUs span eight racks in systems like NVIDIA Vera Rubin Ultra NVL576?

When 576 GPUs span eight racks and operate as a single system — as they will in NVIDIA Vera Rubin Ultra NVL576, which links eight NVLink racks of 72 NVIDIA Rubin Ultra GPUs into one 576-GPU domain — copper can’t carry the signal across that distance. High-bandwidth, low-latency optical interconnects powered by InP-based lasers become mandatory to keep the entire domain coherent. This multi-rack scaling is a primary driver of surging demand for InP substrates used in the laser sources of next-generation AI optical engines.

What makes InP substrates the preferred platform for high-performance semiconductor lasers in AI data centers?

InP’s direct bandgap enables efficient generation of coherent laser light at the exact telecom wavelengths (1.3–1.55 μm) where optical fiber attenuation is lowest, unlike silicon. This allows fabrication of advanced DFB, electro-absorption modulated, and tunable lasers plus full monolithic photonic integrated circuits that combine lasers, SOAs, modulators, and photodetectors on one chip. Virtually every single-mode high-speed transceiver (800G/1.6T and beyond) relies on an InP laser source as the primary optical carrier.

How are InP substrate shortages and new engineered alternatives impacting AI infrastructure scaling in 2026?

Severe InP substrate shortages, concentrated supply among a few players (Sumitomo Electric, AXT, JX Advanced Metals), long lead times, and geopolitical export controls have driven sharp price increases and constrained laser die availability. Engineered solutions such as InP-on-GaAs wafers offer comparable performance, up to ~80% cost savings at scale, and easier scaling to 6-inch+ formats, while major suppliers are investing heavily (e.g., JX’s ¥120 billion capacity expansion). Resolving this bottleneck is now a critical path item for next-generation multi-rack AI systems.