Neon, Krypton & Xenon: The Invisible Specialty Gases Powering AI Chip Manufacturing

- David Rogers

- AI Buildout Supply Chain

- 2026-07-17

In the race to scale AI infrastructure training clusters and edge inference the most advanced chips depend on an invisible foundation: ultra-pure neon, krypton, and xenon. These noble gases, present in air only at parts-per-million levels, enable the excimer lasers at the heart of deep-ultraviolet (DUV) photolithography. Neon dominates ArF laser mixtures (typically ~96% as buffer gas with argon and fluorine) to generate 193 nm light for sub-10 nm patterning, while krypton powers KrF lasers (248 nm) for critical layers on mature and mid-range nodes that still produce the majority of global chip volume /ASML/. Trace xenon appears in certain stabilized mixtures or supports related plasma processes. Without these gases, the multi-patterning and high-volume manufacturing essential for AI accelerators, GPUs, and HBM memory would stall.

Extraction begins in massive cryogenic air separation units (ASUs) tied to steel production or dedicated plants, where air is liquefied and distilled in energy-intensive stages /Linde/. Neon requires processing enormous volumes (~65,000 parts air per part neon); krypton and xenon are even rarer and demand additional enrichment columns. Semiconductor-grade output must reach 5N–6N purity (99.999%+), with oxygen, moisture, nitrogen, and hydrocarbons limited to low parts per billion levels. Any contamination destabilizes the plasma discharge, shortens gas lifetime, risks safety issues, or destroys wafer yields. Specialized blending facilities then create precise excimer mixtures under strict quality control.

The 2022 Ukraine conflict brutally exposed concentration risks: two Ukrainian firms (Ingas and Cryoin) had supplied roughly half the world’s semiconductor-grade neon (and significant shares of krypton/xenon), much of it from Soviet-era steel-mill ASUs /ASN/. Production halts triggered price spikes of 5–10× and forced fabs to burn through 3–6 month stockpiles. The shock accelerated global diversification, with new purification capacity coming online in the US /Air Liquide/, Europe, South Korea /Air Liquide/, and especially China /Yingde/, while chipmakers and gas suppliers invested in resilience.

Demand is accelerating with the AI buildout. DUV remains indispensable alongside EUV for leading-edge logic and memory multi-patterning, and it dominates high-volume trailing-edge production that supports the broader AI ecosystem. A single large fab can consume thousands of cubic meters of neon annually; laser systems refresh gas continuously (roughly 20–30 liters of neon blend per hour per tool) /Photonics Online/. The electronic specialty gases markets expanding in lockstep with AI-driven fab investment.

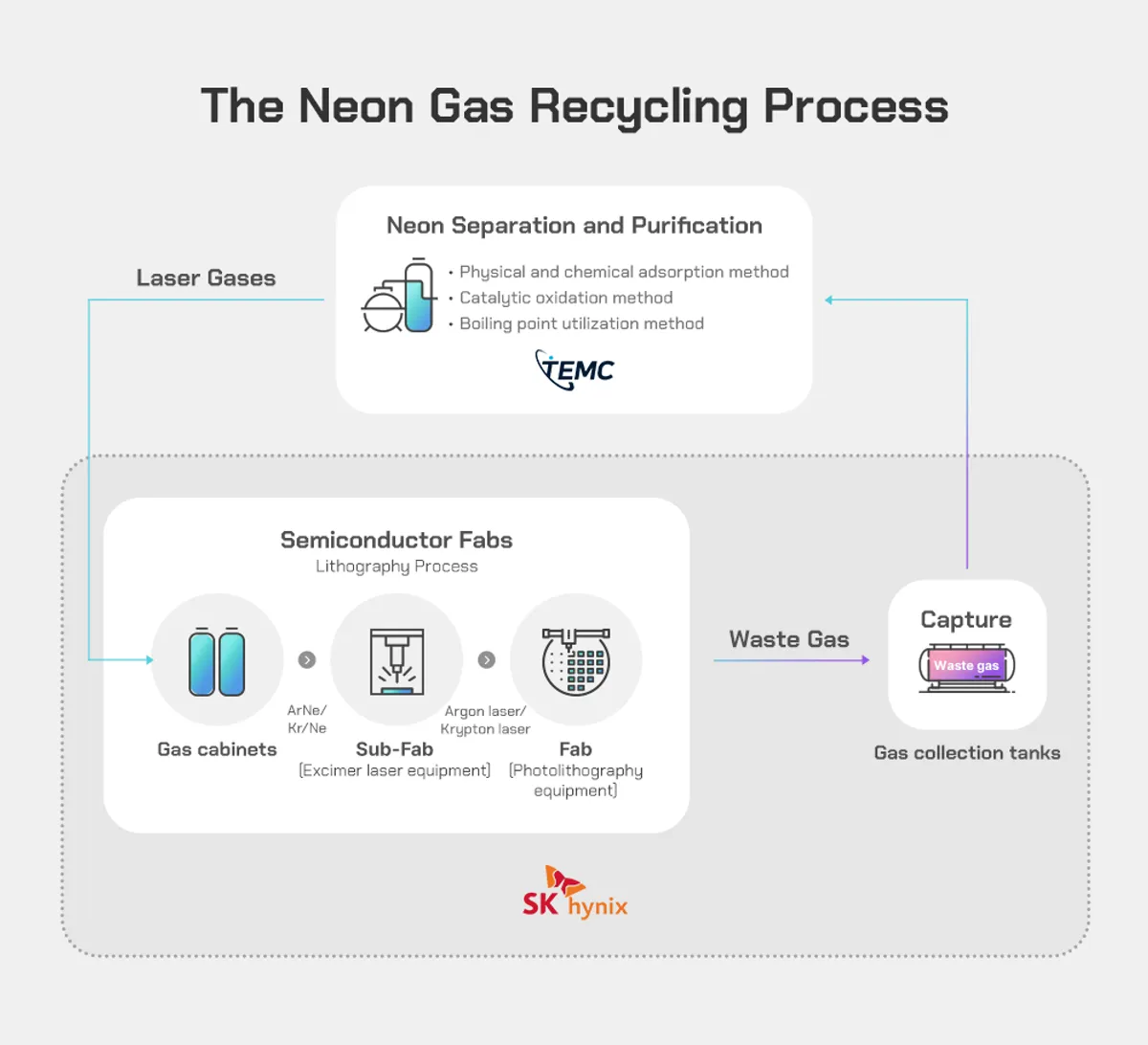

Supply resilience is improving through technology and geography. Global leaders Linde, Air Liquide, and Air Products operate integrated ASU-to-purification chains and are expanding rare-gas capacity, joined by regional players and Chinese producers. On-site neon recycling systems now recover >90% of exhaust gas from excimer lasers /EFC & SK/, dramatically cutting fresh consumption, cost, and waste while easing pressure on primary production. These innovations, combined with new Western and Asian capacity, are mitigating geopolitical and energy-linked risks tied to steel output and concentrated processing know-how. For the AI era, these specialty gases have become strategic infrastructure as critical as the silicon itself.

Key Insights

What are the typical annual volumes of neon, krypton, and xenon consumed in a large semiconductor fabrication plant, and how does planned new fab construction over the next three years proxy future demand for these excimer laser gases?

A large advanced semiconductor fab running 50–100 excimer lasers typically consumes 15,000–20,000 cubic meters of semiconductor-grade neon annually on a gross basis for ArF (~95–96% of the mixture) and KrF DUV lithography, with significantly lower volumes of krypton for KrF and specialized etch processes and only trace xenon in certain stabilized mixtures or niche applications; on-site recycling systems recovering 85–92% or more of the exhaust gas now reduce net fresh consumption to a small fraction of gross usage. Global 300mm fab equipment spending is projected to total $374 billion from 2026 to 2028, with advanced process capacity (7nm and below) growing 69% to reach 1.4 million wafers per month by 2028 amid AI-driven logic and HBM expansion—implying dozens of new or expanded fabs coming online over the next three years as a clear proxy for rising specialty gas demand, even after recycling efficiencies and supplier diversification.

What is the most critical bottleneck in the process technology or supply chain for specialty excimer laser gases like neon, krypton, and xenon in advanced AI chip production?

The primary bottleneck is achieving and consistently maintaining ultra-high purity (5N–6N, with ppb-level control of O₂, H₂O, N₂, and hydrocarbons) during cryogenic air separation, multi-stage purification, precise blending with halogens like fluorine, and closed-loop recycling, all while scaling to meet AI-driven lithography demand. These gases are produced as low-volume byproducts of large ASUs tied to steel output, creating inherent supply inelasticity; new capacity requires 12–18 months lead time and lengthy customer qualification (often 6–12+ months). Recycling systems help but are not universally deployed at leading-edge nodes, and any impurity spike directly risks laser instability, yield loss, or safety issues in high-repetition-rate ArF/KrF tools essential for 3nm-class Rubin GPUs. Geopolitical and energy-linked concentration risks compound the technical constraints even as diversification accelerates.

What are the unit economics of neon, krypton, and xenon specialty gases for semiconductor manufacturing, including long-term supply agreements, cyclicality, and margin growth or defensibility?

These ultra-pure excimer laser gases command high unit value due to extreme purity requirements and scarcity, with suppliers securing long-term agreements (typically 3–5+ years, often bundled with argon, helium, or on-site ASU contracts spanning 15–20 years) that now cover 65–72% of trade and provide revenue stability for producers like Linde, Air Liquide, and Air Products. The business is highly cyclical, tracking semiconductor capex and wafer starts—surging with AI fab builds but contracting sharply in downturns (as seen in 2022–2023 inventory corrections), though long-term contracts and recycling have narrowed price volatility from historical ±25% swings to around ±6%. Margins are structurally attractive and defensible in the electronic-grade segment (often 20–40% operating levels for specialty merchant gases) thanks to high barriers: proprietary purification/blending IP, rigorous fab qualification, on-site recycling technology, and integration with customer facilities, enabling margin expansion as AI demand tightens supply and rewards localized, high-reliability providers.

How have light source manufacturers and the semiconductor industry responded to neon gas shortages affecting excimer laser supply for advanced chip production?

Light source manufacturers such as Cymer and leading chipmakers have countered neon shortages—driven by Ukraine supply shocks that once risked 15%+ cuts and 20× price spikes—through rapid short-term containment solutions and optimized gas-refresh algorithms that reduced consumption by ~30% immediately and up to 50% overall while preserving laser performance, combined with long-term recycling programs that reclaim over 95% of neon from spent ArF/KrF excimer gas via on-site filtration, reconstitution, or supplier return loops. These measures, supported by strategic 1–2 month stockpiles, accelerated qualification of alternative global suppliers, and deeper scientific insight into neon’s essential role in stabilizing (ArF)* plasma for efficient 193 nm DUV lithography, avoided fab shutdowns and delivered industry-wide savings of more than 70 million liters of neon per year (valued at over $200 million), enabling sustained production of advanced nodes critical for AI accelerators even as modern recycling systems now routinely achieve 85–92% recovery.