SiC Power Wafers Powering AI Data Centers: Manufacturing, BPD Challenges & Gen 5 Breakthroughs

- David Rogers

- AI Buildout Supply Chain

- 2026-07-10

Silicon carbide (SiC) power wafers are the critical enabler for the next wave of AI infrastructure. Hyperscale data centers running dense GPU clusters consume staggering amounts of electricity; traditional silicon power devices simply cannot deliver the efficiency, power density, and thermal performance required. SiC MOSFETs and diodes cut switching and conduction losses dramatically (often 50%+ vs. silicon), support higher bus voltages for slimmer distribution architectures, and reduce cooling overhead—directly addressing the power wall facing AI buildouts by hyperscalers /HIITIO/. The same technology is already transforming 800V electric vehicle drivetrains and renewable inverters, but AI data-center power supplies are now emerging as a powerful new growth vector /NVIDIA/.

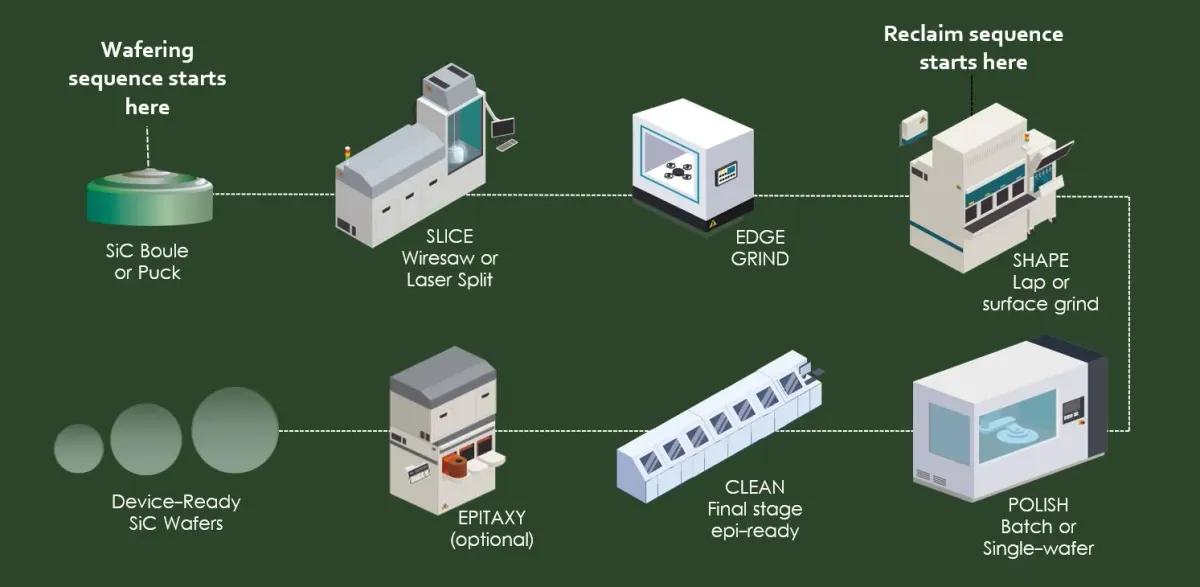

Manufacturing begins with ultra-high-purity SiC powder synthesized from abundant silica sand and carbon sources. The dominant industrial process is Physical Vapor Transport (PVT): the powder is loaded into a graphite crucible and sublimated at temperatures exceeding 2,000 °C under controlled vacuum and temperature gradients /ScienceDirect/. Vapor species (SiC₂, Si₂C, Si) transport and recrystallize onto a precisely oriented 4H-SiC seed crystal, slowly building a single-crystal boule at typical rates of 0.3–2 mm/h typically taking days to weeks. The boule is then ground cylindrical, sliced into wafers via multi-wire diamond sawing (managing kerf loss), lapped, ground, and finished with chemical-mechanical polishing (CMP) to achieve sub-nanometer roughness, extreme flatness, and minimal total thickness variation. Finally, high-temperature CVD epitaxy grows the thin, precisely doped device layers. Purity and crystallographic perfection are non-negotiable; even low densities of micropipes or dislocations destroy device yield and long-term reliability.

Key challenges include the inherently slow, energy-intensive growth and defect proliferation when scaling wafer diameters from today’s dominant 150 mm to 200 mm (and beyond). Among remaining defects, basal-plane dislocations (BPDs) have become the major limiter of long-term device performance and reliability /CS MANTECH/. Overall, larger wafers deliver roughly 30–33% more die per wafer, slashing cost per device once yields stabilize. Material and process advances are already delivering measurable gains, as demonstrated by Wolfspeed’s Gen 5 platform, whose 1200V MOSFETs achieve up to 27% lower specific on-resistance than current competitive solutions /Wolfspeed/. Innovations in thermal management during growth, advanced graphite furnace components, optimized slurries for faster/lower-damage polishing /ScienceDirect/, and emerging laser-based slicing or electrochemical mechanical polishing are all aimed at boosting throughput, cutting energy intensity, and improving yields.

Market momentum is exceptional. The global power SiC device market is forecast to reach approximately $11 billion by 2031, growing at a ~20% CAGR (2025–2031), propelled by EVs, renewables, and—critically—AI data-center power conversion /Yole/. Wolfspeed and others report strong sequential growth in the AI segment as hyperscalers redesign rack and facility power architectures around higher voltages and SiC efficiency. Wafer demand tracks this closely, with the substrate market itself expanding rapidly as device makers secure long-term supply.

Capacity is expanding aggressively while raw-material availability is not a constraint (silica and carbon are abundant; kerf-slurry recycling can recover SiC or produce silica). Wolfspeed remains the clear leader in high-quality substrates (roughly 30–35% share) with major U.S. investments including the Mohawk Valley 200 mm device fab and new crystal-growth facilities /Wolfspeed/. STMicroelectronics, Infineon, and onsemi pursue vertical integration strategies, while Chinese producers (TanKeBlue, SICC, etc.) are scaling rapidly to serve domestic EV and industrial demand. The current capacity build-out race also carries short-term oversupply risk, but the long-term trajectory driven by AI electrification and decarbonization points to sustained, strategically vital demand for secure, high-performance SiC wafer supply.