SOI Wafers: The Critical Substrate Powering Silicon Photonics for AI Data Centers

- David Rogers

- AI Buildout Supply Chain

- 2026-07-09

Silicon-on-insulator (SOI) wafers are the foundational engineered substrate enabling high-performance silicon photonics (SiPh) platforms critical to AI data center scaling. These wafers feature a thin single-crystal silicon device layer atop a buried oxide (BOX) insulating layer on a silicon handle wafer. For SiPh applications, typical specs include a precisely controlled top silicon layer (often ~220–300 nm) and a thicker BOX (commonly 2–3 μm) that provides excellent optical confinement, low propagation loss in waveguides, and electrical isolation /UniversityWafer/. This structure supports monolithic or heterogeneous integration of passive photonic components (waveguides, modulators, mux/demux) alongside electronics, delivering the ultra-high bandwidth, low latency, and energy efficiency needed for optical interconnects replacing copper in hyperscale AI clusters.

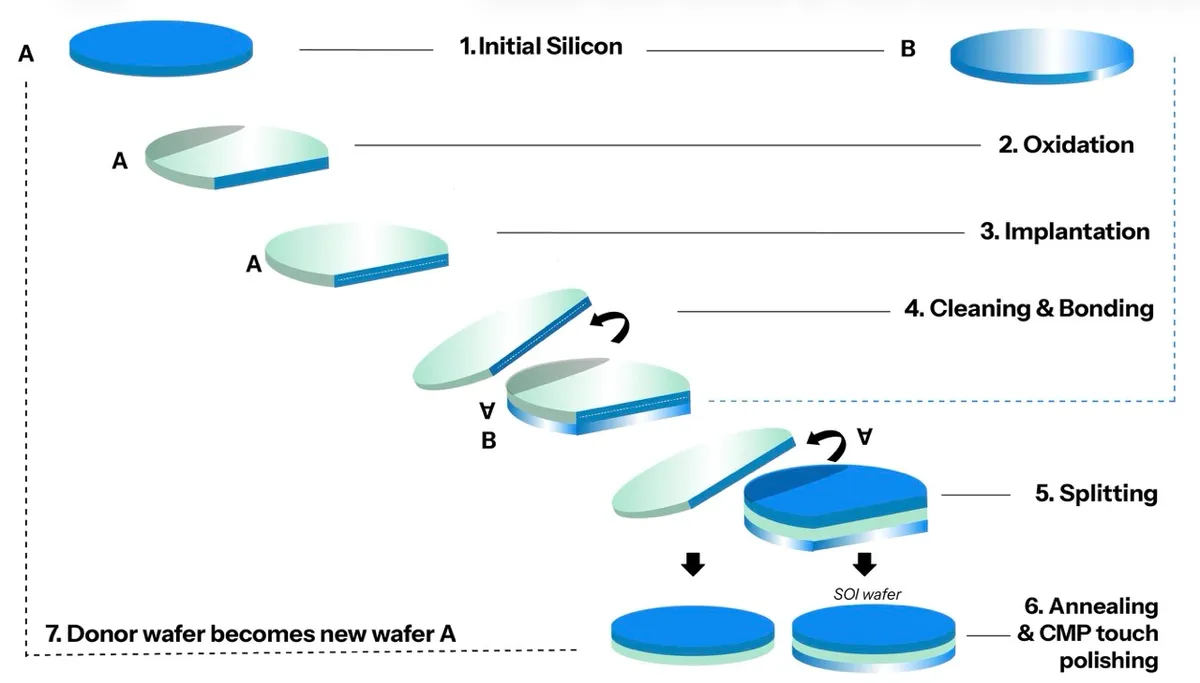

Production relies primarily on Soitec’s proprietary Smart Cut® process (licensed to others), which combines hydrogen ion implantation into a donor wafer, room-temperature hydrophilic bonding to an oxidized handle wafer, controlled thermal splitting to transfer a uniform thin silicon film, and final chemical-mechanical polishing (CMP) plus annealing for surface quality and defect repair /Soitec/. An older alternative, Separation by IMplanted OXygen (SIMOX), uses high-dose oxygen implantation followed by high-temperature annealing to form the buried oxide /ScienceDirect/. Both demand semiconductor-grade purity (sub-ppb metallic impurities, minimal crystal defects) and nanometer-scale uniformity in layer thickness and smoothness are essential for consistent waveguide effective index and minimal scattering losses in photonic circuits.

Key challenges include high manufacturing cost and complexity versus bulk silicon wafers: expensive high-energy ion implanters /Axcelis/, stringent particle/void control in bonding, precise splitting mechanics, and material-intensive CMP. Yield and uniformity on 300 mm wafers remain demanding, especially for photonics-grade low-loss performance across large areas. Emerging solutions focus on process optimizations for higher throughput, improved metrology, fungible capacity reallocation across SOI lines /ResearchGate/, and higher-volume ramps to amortize costs. Recycling of donor wafers or reclaim processes offers limited near-term relief due to the layered structure, though general silicon wafer reclaim (etch/polish) provides cost and waste-reduction pathways for test/monitor material.

Explosive demand is driven by silicon photonics for AI infrastructure including co-packaged optics (CPO), pluggable transceivers (800G/1.6T+), and optical fabrics in data centers and HPC /PhotonCap/. The broader silicon photonics market has a wide range of projections to grow from roughly $2.8–3 billion in 2025 to $9–28 billion by 2030–2034 at CAGRs of 23–29%, with AI/cloud workloads as the primary accelerator. Photonics-SOI substrates are the starting material for leading foundry platforms, enabling the power savings (up to 30% in some architectures) and density required as electrical interconnects hit physical limits.

Supply is highly concentrated. Soitec (France) dominates with its Smart Cut IP portfolio and near-monopoly position in photonics-grade SOI at meaningful scale; its Bernin and Singapore facilities support 200/300 mm production /Soitec/, with new tooling underway for 300 mm Photonics-SOI and fungible capacity that can be redirected as CPO/1.6T ramps accelerate (Photonics-SOI revenue already approaching €100 million scale). GlobalWafers (via MEMC in Missouri) is ramping U.S. 300 mm SOI production with CHIPS Act support, creating a key domestic source /NIST/. Shin-Etsu (Japan) also produces licensed SOI.

As AI buildout intensifies optical interconnect deployment, SOI wafer supply, led by Soitec’s technology moat and selective geographic diversification, will be a critical pacing item. Continued yield gains, capacity activation, and strategic inventory management will determine how smoothly the industry scales the photonic layer of the AI stack.