300mm Silicon Wafers: The Precision Foundation Powering AI Chip Production

- David Rogers

- AI Buildout Supply Chain

- 2026-07-08

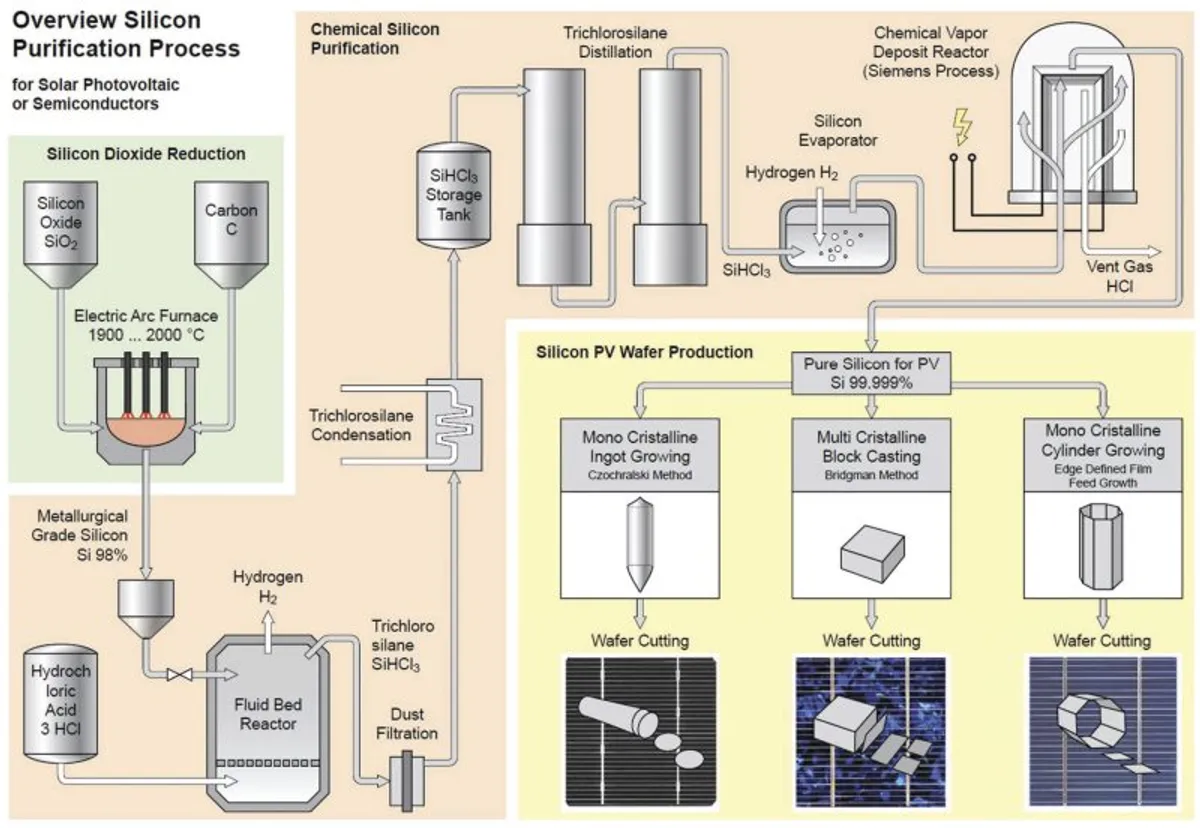

Every advanced AI accelerator, GPU, and high-bandwidth memory chip begins life on a 300mm silicon wafer, a near-atomically flat, defect-free single-crystal disk /NIST/. Production starts with abundant quartz sand reduced to metallurgical-grade silicon, then purified to electronic-grade polysilicon (typically 9N–12N purity, or 99.9999999%+). Specialists like Wacker Chemie (Europe’s leader in hyperpure semiconductor-grade polysilicon) supply this feedstock /Wacker/. It is melted in a quartz crucible at ~1,414 °C inside a Czochralski (CZ) puller; a seed crystal is dipped, rotated, and slowly withdrawn to grow a massive dislocation-free boule. The ingot is cropped, ground, diamond-wire sliced, edge-profiled, lapped, etched, and chem-mechanically polished to nanometer flatness and sub-parts-per-billion metallic purity— capabilities that directly determine yields at 3 nm, 2 nm, and beyond.

The core challenges are technical and economic. Controlling oxygen incorporation from the crucible, dopant uniformity across 300mm diameters, and grown-in defects (COPs, slip) becomes exponentially harder at leading-edge nodes /SSRN/. Slicing still incurs ~40% kerf loss /Zelatec/; while diamond-wire technology and reclaim/recycling pilots recover material for solar or lower-grade use, closed-loop semiconductor-grade recovery remains limited and costly. Energy intensity of CZ growth and the multi-billion-dollar capex for new capacity add pressure. The industry has largely deprioritized 450 mm wafers /SemiWiki/ due to equipment scale-up costs, instead squeezing more value from 300mm through faster pull rates, better hot-zone design, automation, and ultra-flat specifications tailored for EUV and chiplet architectures.

Demand is tightly coupled to the AI buildout. 300mm wafers already represented over 64% of global silicon wafer area shipments (which reached ~12,266 MSI in 2024 and rebounded ~5–6% in 2025). AI accelerators, HPC logic, HBM, and advanced packaging are the primary drivers, with foundries and memory makers expanding capacity aggressively. Analysts project 5–7% CAGR for the silicon wafer market through the early 2030s as data-center and edge-AI silicon demand compounds /Fortune Business Insights/.

Supply is highly concentrated. Japan’s Shin-Etsu and SUMCO together supply roughly 50–54% of global 300mm wafers /Brookings/; the top five producers (adding GlobalWafers of Taiwan, Siltronic of Germany, and SK Siltron of Korea) control ~82–85%. Raw quartz is plentiful worldwide, but the know-how and capital for large-diameter, low-defect crystal growth create real bottlenecks. Wafer reclaim and kerf recycling provide marginal relief but do not meaningfully displace primary production. Geopolitical concentration risks are material: East Asia dominates both production and consumption (especially Taiwan’s advanced fabs), while China leads overall polysilicon capacity (mostly solar-grade) and is expanding domestic wafers under state support. Allied export controls on equipment and CHIPS Act-driven U.S. investments /Reuters/ are actively reshaping the map toward greater resilience.

For the AI industrial buildout, 300mm silicon wafers are foundational infrastructure. Without reliable volumes of these ultra-precise substrates, the GPUs and custom ASICs powering the next wave of intelligence cannot scale. Ongoing Japanese technology leadership, selective reshoring, process innovation to cut waste and cost, and diversified capacity will determine whether the physical layer keeps pace with AI’s software-defined ambitions.