Boron: The 1% Element Powering High-Performance NdFeB Magnets in AI Data Centers

- David Rogers

- AI Buildout Supply Chain

- 2026-07-03

NEED TO KNOW

- Essential 1% Magnet Stabilizer: Boron constitutes 1–1.2% by weight of NdFeB magnets, stabilizing the tetragonal Nd₂Fe₁₄B crystal phase to deliver unmatched coercivity and thermal stability.

- Geographically Diversified Mining: Unlike rare earths, raw boron mining is robustly anchored in Turkey (73% of reserves via Eti Maden) and the US (Rio Tinto's U.S. Borax in California).

- Downstream Magnet Concentration: While upstream mining is diversified, downstream ferroboron alloying and NdFeB magnet sintering remain 90%+ concentrated in China.

- Surging AI Data Center Storage: Skyrocketing AI dataset storage demands have cleared out enterprise HDD capacity, driving strong offtake for high-purity ferroboron feedstocks.

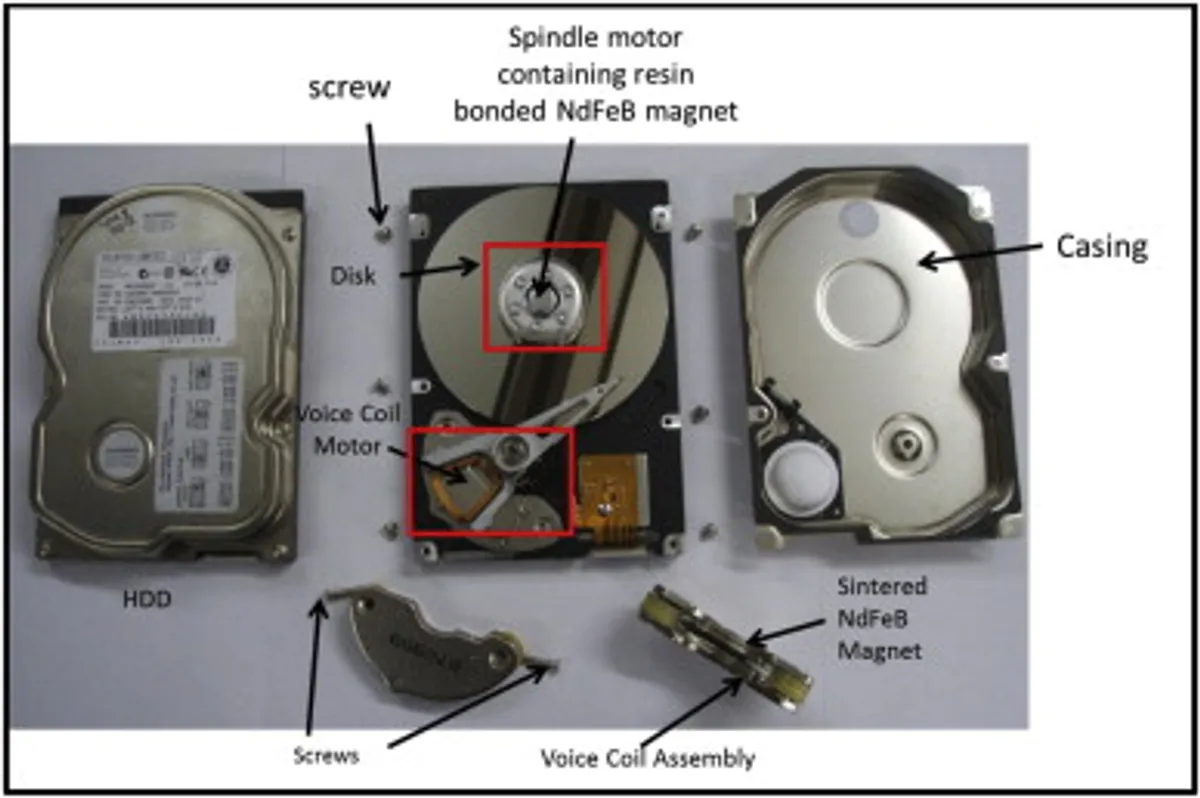

Sintered NdFeB (neodymium-iron-boron) permanent magnets are the workhorses powering HDD spindle motors/actuators, server cooling fans, and precision motors across AI infrastructure. Boron is the essential 1–1.2% by weight that makes everything possible /Stanford Magnets/. Boron’s unique properties provide stability to the tetragonal Nd₂Fe₁₄B crystal phase delivering unmatched magnetic strength, coercivity, and thermal stability required for compact, high-performance, energy-efficient designs in data centers and beyond. Invented in the early 1980s, these magnets now dominate ~95%+ of the permanent magnet market outclassing older ferrite, AlNiCo, and Samarium-Cobalt (SmCo) options.

Boron enters magnet production primarily as ferroboron alloy or elemental boron, derived from high-purity boric oxide or boric acid refined from borate minerals (kernite, tincal, colemanite, ulexite). The upstream process of mining, conversion to refined borates, then controlled reduction or alloying demands exceptional purity and particle-size consistency. Impurities can degrade final magnet properties during vacuum induction melting, strip casting, and sintering/powder metallurgy. U.S. Borax (Rio Tinto’s California operation) is a standout Western supplier of these high-purity, consistent inputs critical for reliable magnet production /Borax/.

Global boron resources are abundant and geopolitically diversified compared with rare earths. Turkey holds ~73% of global reserves and leads refined borate production (Eti Maden, state-owned, ~50% share) /MDPI/. The United States (Rio Tinto Boron mine) is a major Western producer with very low net import reliance (~3.8% in recent data). Other contributors include Argentina, Bolivia, Chile, Peru, China, and Russia. USGS data confirm world resources are adequate for the foreseeable future; the US added boron to its 2025 Critical Minerals List /USGS/. Recycling is currently insignificant overall, though emerging NdFeB magnet recycling (focused on rare earths Neodymium and Dysprosium) may eventually yield boron as a byproduct.

Technical and cost challenges center on efficient, high-purity ferroboron production at scale while minimizing energy use, waste, and impurities. Emerging efforts from companies like 5E Advanced Materials have identified two redox-based (reduction-oxidation) process routes for mine-to-magnet optimization, alternative precursors, and domestic capacity /ACCESS Newswire/. Demand tailwinds are strong: AI data center buildout is driving HDD and cooling fan needs (with reported shortages and price pressure) /PCMag/, layered on top of robust growth from EVs, wind turbines, and precision industrial motors. NdFeB market expansion supports steady boron offtake in this high-spec niche, even if magnets represent only a small fraction of total boron consumption.

Upstream leaders include Eti Maden (Turkey) and U.S. Borax (US) for refined borates and high-purity inputs; ferroboron and magnet alloying/sintering remain more concentrated, with China holding ~90%+ of global sintered NdFeB production /BIS/. This creates indirect supply-chain risk for Western users despite boron mining diversification. Firms advancing non-Chinese magnet capacity (e.g., MP Materials, USA Rare Earth efforts in the US; European and Japanese players) rely on secure boron feedstock like that from U.S. Borax. As AI infrastructure scales, boron’s reliable, high-purity supply will be foundational to de-risking the precision magnets that keep data centers running efficiently. Boron may be small in the magnet recipe, but it is mighty for the AI era.

Key Insights

What is the function of boron in neodymium-iron-boron (NdFeB) permanent magnets?

Boron constitutes 1% to 1.2% by weight of NdFeB magnets, stabilizing the tetragonal Nd₂Fe₁₄B crystal structure to maximize magnetic strength, coercivity, and thermal stability. This allows the magnets to perform reliably in high-temperature environments, such as HDD spindle motors and server cooling fans within AI data centers.

Which countries control the global mining and refining of boron?

Turkey holds approximately 73% of global boron reserves, with its state-owned company Eti Maden managing about 50% of refined borate production. The United States is also a major producer, primarily through Rio Tinto’s U.S. Borax operations in California, which provides high-purity inputs for industrial magnet manufacturing.

What are the supply chain risks for boron inputs used in AI hardware?

Although raw boron mining is geographically diversified between Turkey and the United States, downstream ferroboron alloying and NdFeB magnet sintering are highly concentrated in China, which controls over 90% of global production. This concentration creates indirect supply risks for Western AI infrastructure developers relying on advanced permanent magnets.