Neodymium Magnets: Powering AI Data Centers, Chip Manufacturing & the Supply Chain

- David Rogers

- AI Buildout Supply Chain

- 2026-07-02

NEED TO KNOW

- Essential for High-Efficiency Cooling: Neodymium (NdFeB) permanent magnets power compact brushless DC motors for cooling fans, pumps, and liquid loops in dense 100kW+ GPU racks.

- Sub-Nanometer Lithography Levitation: ASML TWINSCAN DUV/EUV wafer stages rely on massive NdFeB magnet Halbach arrays and Lorentz actuators to achieve quarter-nanometer positioning accuracy under multi-g acceleration.

- China Processing Dominance: China controls ~60% of REE mining, 91% of refining, and 94% of NdFeB magnet manufacturing, creating severe concentration risks for Western tech.

- Western Mine-to-Magnet Ramp: MP Materials (Mountain Pass & Texas) and Noveon Magnetics are establishing domestic separation, magnet sintering, and commercial recycling capacity.

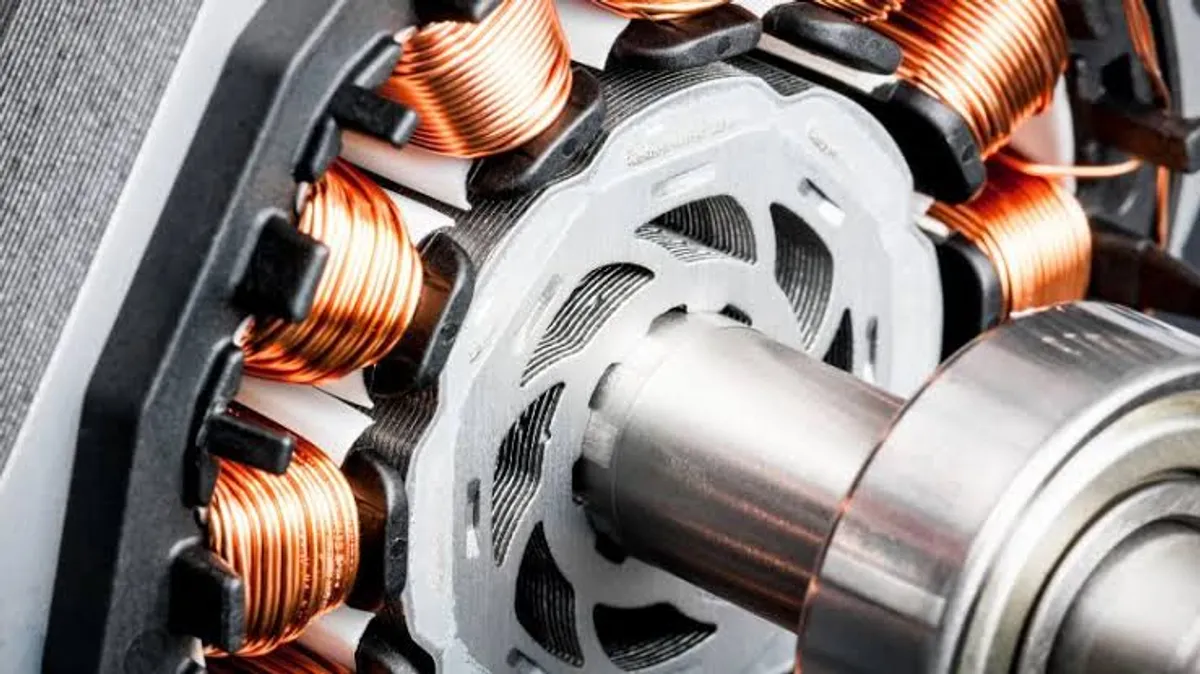

Neodymium (Nd) is the essential rare earth element enabling the strongest commercial permanent magnets made of neodymium-iron-boron (NdFeB). These magnets drive high-efficiency motors and generators critical to the AI revolution. In hyperscale data centers, NdFeB magnets power compact, energy-saving brushless DC and permanent-magnet synchronous motors in cooling fans, pumps, blowers, and liquid-cooling loops /Qorvo/. As GPU/TPU clusters generate massive heat in dense racks, these magnets help minimize power consumption and ensure reliability—directly supporting the explosive growth of AI compute.

Extracting and refining neodymium starts with bastnasite or monazite ores, which undergo crushing, flotation to ~60% rare earth ore (REO) concentrate, acid leaching, and then multi-stage solvent extraction /Britannica/. Chemically similar rare earths require hundreds (sometimes over 1,000) of mixer-settler stages for separation into individual elements or optimized Nd-Pr-Dy mixes. High purity (typically >99.5% for oxides or metals) or precise alloying is needed for magnetic performance, though research shows high-quality magnets can use somewhat lower-purity or mixed feeds. The process is capital-intensive, energy- and water-heavy, and generates acidic/toxic waste streams which are key technical and environmental challenges driving innovation in shorter flowsheets, new extractants, membranes, and direct alloy routes.

Demand for neodymium is surging across motors and a wide range of industrial magnetic systems. Magnet rare earths (Nd, Pr, Dy, Tb) have seen demand double since 2015 and are projected to grow another third by 2030, driven by EVs, wind turbines, and AI data center cooling that depends on precision permanent-magnet motors for efficient thermal management . Beyond motors, neodymium is central to complex electro-magnets for secure, low-power precision workholding like ASML’s TWINSCAN dual-stage wafer positioning technology (used across DUV and EUV platforms) which relies on magnetically levitated wafer stages that achieve accelerations of several g’s while maintaining positioning accuracy down to a quarter of a nanometer. These applications underscore neodymium’s role in compact, reliable motion control and material handling which is vital for both AI hardware manufacturing and the broader industrial base enabling the AI buildout. The NdFeB magnet market continues its strong expansion as a result.

Demand for neodymium is surging across motors and a wide range of industrial magnetic systems. Magnet rare earths (Nd, Pr, Dy, Tb) have seen demand double since 2015 and are projected to grow another third by 2030, driven by EVs, wind turbines, and AI data center cooling that depends on precision permanent-magnet motors for efficient thermal management /Adamas/. Beyond motors, neodymium is central to complex electro-magnets and hybrid permanent-magnet systems for secure, low-power precision workholding and motion control. A prime example is ASML’s TWINSCAN dual-stage wafer positioning technology (used across DUV and EUV platforms), which relies on magnetically levitated wafer stages achieving accelerations of several g’s while maintaining positioning accuracy down to a quarter of a nanometer. These systems use large permanent-magnet plate arrays (including Halbach configurations with thousands of NdFeB magnets) and Lorentz-force/voice-coil actuators /Entropy Capital/. These applications underscore neodymium’s role in compact, reliable motion control and material handling—vital for both AI hardware manufacturing and the broader industrial base enabling the AI buildout. The NdFeB magnet market continues its strong expansion as a result.

On the supply side, global rare earth mine production reached ~390,000 tonnes REO equivalent recently, with China controlling ~60% of magnet rare earth element (REE) mining, 91% of refining, and 94% of permanent magnet production. Western capacity is scaling: MP Materials (Mountain Pass, US) reported record NdPr output in early 2026 and is building full domestic separation-to-magnet capability (Texas facilities targeting thousands of tonnes annually, with major expansion later this decade) /MP Materials/. Lynas Rare Earths (Australia/Malaysia) is expanding light and heavy REE separation. Recycling remains under 1% today but is growing via urban mining from end-of-life motors, HDDs, and electronics; companies like Noveon Magnetics (US) and HyProMag are pioneering commercial recovery and remanufacture /HyProMag/.

Geopolitical concentration creates real risks that are exacerbated by China’s 2025 export controls and licensing on heavy REEs and certain magnets, which caused delays into 2026. Leading non-Chinese players (MP Materials with DoD support, Lynas, and emerging magnet makers like Arnold Magnetic Technologies) are critical to diversification /Arnold/. For the AI buildout to proceed resiliently and at scale, accelerating mine-to-magnet chains outside China, plus higher recycling rates, is a strategic priority. Neodymium is foundational industrial technology for the compute era.

Key Insights

How do neodymium magnets support AI data center cooling systems?

Neodymium-iron-boron (NdFeB) permanent magnets power high-efficiency brushless DC and synchronous motors used in cooling fans, water pumps, and liquid-cooling loops. By delivering high magnetic strength in compact designs, these magnets minimize power consumption and ensure reliability in the dense, high-heat environments created by GPU clusters.

Why is neodymium critical for ASML EUV lithography machines?

Neodymium is used in large permanent-magnet arrays and Lorentz-force actuators to levitate and position wafer stages in ASML's DUV and EUV lithography machines. These magnetic positioning systems enable the wafer stage to accelerate rapidly while maintaining sub-nanometer alignment accuracy, which is essential for printing nanoscale features on advanced AI chips.

What steps are being taken to establish a non-Chinese supply of neodymium magnets?

MP Materials is expanding its Mountain Pass facility in California to separate neodymium-praseodymium (NdPr) and is building domestic magnet manufacturing plants in Texas. In addition, recycling startups like Noveon Magnetics and HyProMag are scaling commercial recovery processes to reclaim NdFeB magnets from end-of-life electronics and industrial motors.