Copper in AI Data Centers: Power Delivery, Chip Interconnects & the 800V Shift

- David Rogers

- AI Buildout Supply Chain

- 2026-06-29

NEED TO KNOW

- BEOL & Infrastructure Conductor: Copper forms the damascene-electroplated interconnects in sub-10nm chips and dominates data center power delivery (20–33 tonnes of copper consumed per MW of AI compute).

- The 800V DC Architecture Shift: Transitioning facility power from AC to 800V DC cuts in-rack copper conductor volume and weight by up to 75% while making megawatt-scale racks feasible.

- Sulfuric Acid Market Indicator: Sulfuric acid, a key smelting byproduct, has emerged as a primary price signal and operational bottleneck for copper heap leaching in major mining regions like Chile.

- Electromigration & Resistance Limits: At 2nm nodes, narrow line widths cause sharp electron scattering and resistivity spikes, driving research into hybrid metallization and alternative barrier layers.

Copper’s exceptional electrical conductivity, thermal performance, and reliability make it non-negotiable for AI infrastructure. In advanced semiconductor nodes, it forms the multilayer back-end-of-line (BEOL) interconnects that wire billions of transistors together via damascene electroplating. In data centers, it dominates power delivery through busbars, cables, connectors, and grounding systems that handle extreme densities (AI racks often exceeding 100 kW). A single large data center can consume thousands of tonnes of copper; industry benchmarks show roughly 20–33 tonnes per megawatt (MW) of load /BHP/ for power networks, cooling integration, and other hardware.

Primary production begins with mining and flotation concentration, followed by smelting to copper matte, converting, fire refining, and electrolytic refining to yield 99.99% pure cathodes. Bioleaching, the process of using specialized bacteria to solubilize copper from low-grade ores and tailings, and solvent extraction-electrowinning (SX-EW) hydrometallurgical processes /Metso Outotec/ are gaining traction as lower-energy, lower-emission eco-friendly alternatives to traditional high-temperature smelting, especially as ore grades decline and sustainability pressures mount. For semiconductor interconnects and sputtering targets used in chip fabrication, producers apply additional vacuum distillation, directional solidification, or zone refining to reach 5N (99.999%) to 6N+ (99.9999%+) purity. These ultra-low impurity levels (especially sulfur, oxygen, and metallic contaminants) are essential to prevent electromigration, voids, and defects in sub-10 nm lines and to maintain resistivity close to bulk copper in narrow trenches.

Key technical challenges span both supply and application. On the production side, declining ore grades, water scarcity in major mining regions, long permitting timelines (often 10–17 years from discovery to output), and high capital intensity slow new supply growth /S&P Global/. In chips, copper interconnects at 2nm and smaller become so narrow that resistivity rises sharply from electron scattering at surfaces and grain boundaries. The thin barrier and liner layers needed to contain the copper also take up a larger share of the limited space, increasing signal delay and long-term reliability risks. Data-center power delivery faces density and thermal constraints that make aluminum substitution impractical in dense racks as copper’s superior conductivity and heat handling remain essential even as active electrical cables and advanced digital signal processors push copper’s reach and efficiency for short-reach AI cluster interconnects.

However, emerging 800 Volts direct current (VDC) data center architectures, led by Nvidia for next-generation AI factories /NVIDIA/, are set to reshape copper needs in power delivery. Facility-level conversion from medium-voltage alternating current (AC) creates an 800 VDC backbone distributed directly to racks via simplified three-wire busways and cabling. Due to Watt’s Law P = I × V, the same conductor cross-section carries 157% more power than 415 VAC systems while resistive (I²R) losses drop sharply. Analyses show copper conductor volume and weight can be cut by up to 45% overall, and in-rack copper by as much as ~75% in high-density designs through thinner gauges, fewer parallel conductors, and smaller connectors. A traditional 48 VDC 1MW rack might demand over 200kg of copper cabling (impractical in bulk and losses); 800 VDC makes megawatt-scale racks feasible with far less material, freeing space for denser compute and lowering installation costs.

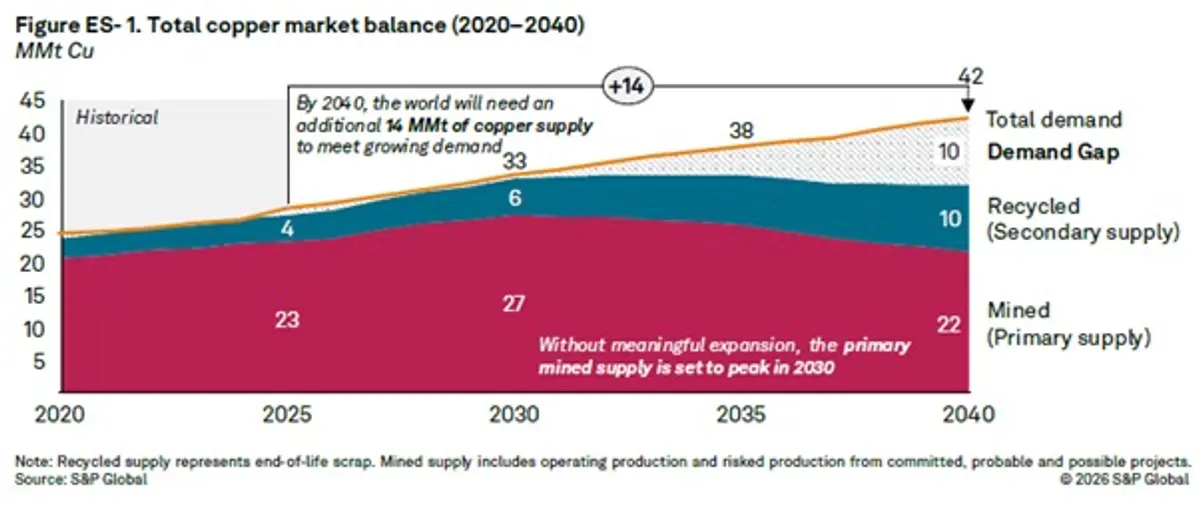

Ultimately, global copper demand is projected to rise ~50% to around 42 million tonnes by 2040, with AI and data centers as a major new vector adding significant incremental volume /S&P Global/. Data-center-specific copper consumption could reach several hundred thousand tonnes annually in the coming decade. Reserves are ample (hundreds of millions of tonnes), and recycling already supplies 30–35% of refined copper with near-infinite recyclability without quality loss, yet end-of-life collection rates remain low (~32% globally) and formal e-waste recycling lags. Primary mine production hovers near 23 million tonnes annually with limited near-term growth. At the same time, sulphuric acid, a major byproduct of copper smelting, is emerging as a new leading indicator of supply conditions /Mining.com/. Sharp rises in acid prices, particularly in China, have boosted smelter margins and are now influencing concentrate valuations and production decisions, while acid supply disruptions can directly constrain leaching operations in key regions like Chile.

Major mining firms include Codelco (Chile), BHP, and Freeport-McMoRan, while high-purity refining and semiconductor-grade copper (targets, interconnect materials) are led by Japanese specialists such as JX Advanced Metals and Mitsubishi Materials, alongside Aurubis in Europe. China has expanded smelting capacity far faster than the miners can deliver ores /Reuters/, creating supply-chain chokepoints even as ore mining is more diversified across Chile, Peru, Australia, and the DRC. Geopolitical risks such as resource nationalism, labor disruptions, trade tensions, and climate impacts on key producers underscore the need for accelerated recycling, diversified refining, and new primary projects to support the AI buildout without bottlenecks. Copper remains the foundational conductor enabling AI’s explosive growth; scaling its responsible supply is now a strategic industrial priority.

Key Insights

How is copper utilized in AI chip fabrication and data center infrastructure?

Copper is used to form back-end-of-line chip interconnects via electroplating and serves as the primary conductor in data center power distribution systems, including busbars, cables, and connectors. Because AI data center racks often exceed 100 kilowatts, a single facility can consume thousands of tonnes of copper, utilizing roughly 20 to 33 tonnes per megawatt of load.

How does the shift to 800V DC power architectures impact copper consumption in AI data centers?

Transitioning to 800 Volts direct current (800 VDC) architectures reduces copper volume and weight by up to 45% in power networks, and by up to 75% inside data center racks. By operating at higher voltages, the system lowers current requirements, which reduces resistive energy losses and allows engineers to use thinner copper gauges and smaller connectors.

What role does sulfuric acid play in the global copper supply chain?

Sulfuric acid is a major byproduct of copper smelting and has emerged as a key price indicator for the copper market. Rising sulfuric acid prices boost smelter margins and influence copper concentrate valuations, while acid supply disruptions can directly limit heap leaching operations used to extract copper from low-grade ores in mining regions like Chile.