Starting a Wafer: High-Purity Quartz from Spruce Pine and Silicon Powering AI Chip Production

- David Rogers

- AI Buildout Supply Chain

- 2026-06-26

NEED TO KNOW

- Single-Source Crucible Chokepoint: Spruce Pine, NC mines supply 70–90% of global semiconductor-grade high-purity quartz (HPQ), which is mandatory for producing the fused quartz crucibles used to pull single-crystal silicon ingots.

- Czochralski (CZ) Process Dependency: Electronic-grade polysilicon (9N–11N purity) is melted at >1,425 °C in HPQ crucibles; any crucible contamination introduces metallic defects that ruin sub-10nm transistor yields.

- Record Wafer Start Growth: Surging AI compute demand is projected to lift global silicon wafer shipments to a record 15,485 million square inches by 2028.

- Geographic Disconnect: Raw HPQ is mined in the US (Sibelco, The Quartz Corp), but ~93% of polysilicon refining is in China and >50% of advanced 300mm wafer manufacturing is controlled by Japan's Shin-Etsu and SUMCO.

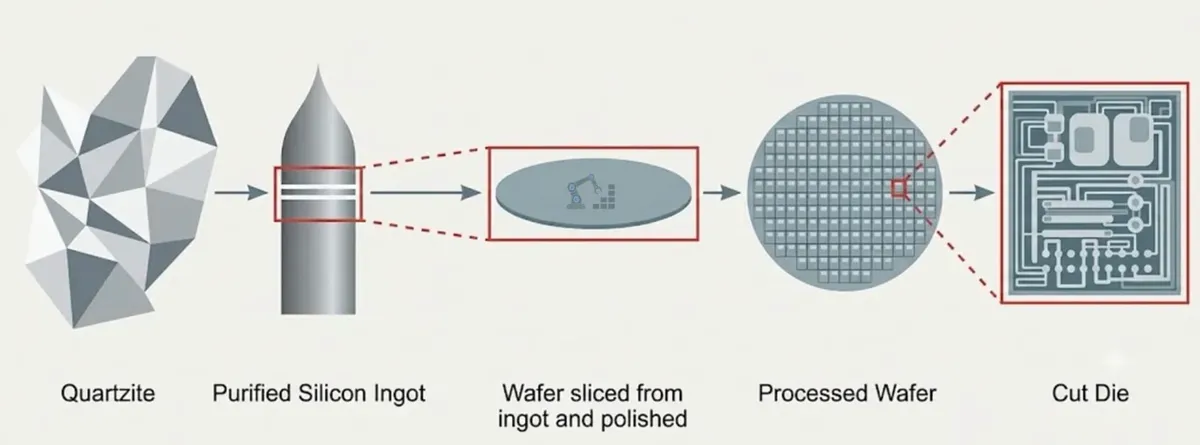

Silicon remains the essential base material for all semiconductor wafers, but producing the flawless single-crystal ingots required for advanced AI chips depends equally on an ultra-specialized input: high-purity quartz (HPQ) converted into fused quartz crucibles. The journey starts with quartz sand reduced to metallurgical-grade silicon, then chemically refined (typically via the Siemens process) into electronic-grade polysilicon at 9N–11N purity /Coreshell/. This polysilicon is melted in HPQ-derived crucibles during the Czochralski (CZ) process at over 1,425 °C under argon; a seed crystal is pulled to grow massive single-crystal ingots that are sliced into wafers. Without these exceptionally pure crucibles, metallic impurities would contaminate the melt and destroy transistor performance at advanced nodes.

The world’s premier source of this HPQ lies in the Spruce Pine Mining District of North Carolina. Two uniquely pure ore bodies there supply an estimated 70–90% of global high-purity quartz suitable for semiconductor-grade fused quartz products. Sibelco (Belgium-based) operates the leading facilities producing its IOTA® HPQ brand and is investing $200 million to roughly double capacity, with completion targeted for 2025 and supported by mine-life potential exceeding 100 years /Sibelco/. The Quartz Corp, a joint venture between Imerys (France) and Norsk Mineral (Norway), operates the second major Spruce Pine facility. Almost all output is processed into crucibles and other high-tech components and exported primarily to Asian semiconductor and solar markets.

Key technical challenges span both materials. Polysilicon refining and CZ growth are extremely energy-intensive, with strict contamination control needed at parts-per-billion levels. HPQ mining and processing must maintain geological purity while scaling output; any shortfall in crucible supply directly constrains ingot and wafer production. Emerging solutions include more efficient fluidized-bed reactors for polysilicon /REC Silicon/, larger 300/450 mm ingots to improve economics /The Electrochemical Society/, energy-recovery systems in CZ pullers, and expanded HPQ capacity. Recycling of silicon kerf and end-of-life crucibles is advancing but remains secondary to primary supply.

AI is the dominant driver of demand, measured directly in wafer starts, the volume of silicon wafers initiated in fabrication plants. Global silicon wafer shipments (a close proxy for production driven by wafer starts) are projected to rise 5.4% in 2025 to 12,824 million square inches (MSI), with a new industry record of 15,485 MSI expected by 2028 /SEMI/. Leading-edge logic for AI accelerators, high-bandwidth memory (HBM), and data-center infrastructure accounts for a growing share of these advanced-node wafer starts, amplifying demand for both ultra-pure polysilicon and the HPQ crucibles essential to every CZ run. At the same time, solar PV demand continues to consume the large majority of overall polysilicon production volume, sustaining upstream capacity that also supports semiconductor supply chains, while optical fiber and high-performance quartz lighting represent additional meaningful end-markets for HPQ-derived fused quartz products.

Supply concentration creates strategic tension. Spruce Pine HPQ offers a U.S.-controlled resource (with Sibelco as the clear leader alongside The Quartz Corp), yet most crucibles ultimately support Asian fabs. Polysilicon capacity remains heavily concentrated in China (~93% of global output), while advanced wafer production is led by Japanese firms (Shin-Etsu and SUMCO together hold over 50% of leading-edge capacity) and Taiwanese/GlobalWafers players. Recent natural-disaster disruptions at Spruce Pine underscored vulnerability /CNBC/. Western onshoring via the CHIPS Act and capacity expansions aim to diversify the chain, while the raw abundance of quartz globally supports long-term scalability, provided the specialized HPQ and high-purity silicon processing keep pace with AI-driven wafer-start growth.

Key Insights

Why is high-purity quartz from Spruce Pine, North Carolina, critical for silicon wafer manufacturing?

High-purity quartz from Spruce Pine is processed into fused quartz crucibles used in the Czochralski process to melt polysilicon at temperatures exceeding 1,425 °C. Because Spruce Pine mines supply 70% to 90% of the world's semiconductor-grade high-purity quartz, any supply disruption there immediately threatens the production of single-crystal silicon ingots globally.

How does the Czochralski process convert polysilicon into semiconductor-grade silicon wafers?

The Czochralski process involves melting electronic-grade polysilicon of 9N to 11N purity inside a fused quartz crucible and dipping a seed crystal into the melt. As the seed is rotated and slowly withdrawn, it grows into a single-crystal silicon ingot, which is subsequently sliced and polished into the ultra-pure wafers used for AI chip fabrication.

What are the main geopolitical risks in the silicon wafer supply chain?

The silicon wafer supply chain is highly concentrated, with China producing about 93% of global polysilicon and Japanese firms Shin-Etsu and SUMCO controlling over 50% of advanced wafer manufacturing. While the raw quartz is mined in the United States, most refining and wafer production occurs in Asia, exposing the AI hardware supply chain to geopolitical and natural disaster risks.