Tantalum Capacitors Powering AI Servers: Supply Chain Challenges, Refining Process & Niobium Alternatives

- David Rogers

- AI Buildout Supply Chain

- 2026-06-24

NEED TO KNOW

- Critical GPU Power Decoupling: Tantalum polymer capacitors provide high volumetric efficiency (CV/g) and ultra-low ESR for localized power delivery, with a single 18-tray AI server rack utilizing up to 7,200 bulk capacitors.

- Geopolitical & ESG Extraction Risks: Over 50% of raw tantalum mine output originates from the DRC and Great Lakes region of Africa, creating significant ethical, ESG compliance, and supply disruption risks.

- Powder Processing Oligopoly: Refining capacitor-grade tantalum (99.99% purity) is controlled by upstream processors like Global Advanced Metals (GAM) and downstream capacitor leaders KEMET (Yageo), AVX, Vishay, and Panasonic.

- Design Alternatives: To manage cost and supply lead times (20–30+ weeks), hardware engineers blend MLCCs, polymer aluminum, and niobium oxide capacitors, reserving tantalum where extreme thermal and ripple performance is non-negotiable.

In the race to build out AI infrastructure, data centers and GPU servers demand rock-solid power delivery networks. Tantalum capacitors, with their unmatched volumetric efficiency, low ESR, and exceptional reliability under high ripple currents and temperatures /Utmel/, are increasingly vital on AI accelerator cards and server motherboards for decoupling and filtering. Surging demand from hyperscalers has already triggered repeated price increases and tighter availability (often exceeding 20–30 week lead times) as manufacturers run near capacity.

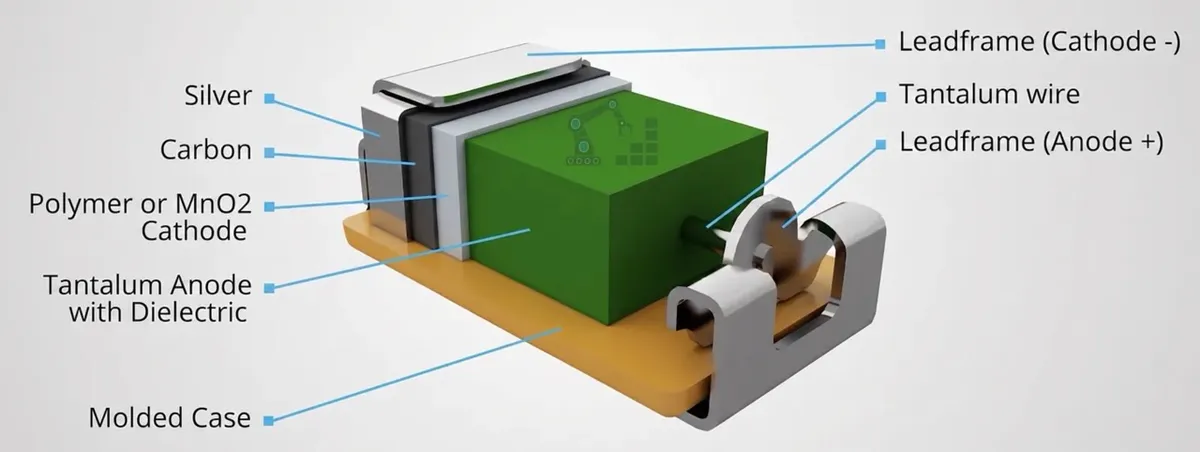

Producing capacitor-grade tantalum is a multi-stage industrial feat requiring purities of 99.99% or higher and precise powder morphology. Ore (often coltan) is beneficiated to concentrates, then subjected to hydrometallurgical refining /Springer/: acid leaching (frequently involving HF), solvent extraction to separate tantalum from niobium, purification to salts, and reduction/processing into high-purity powders with tailored morphology for porous anode sintering and anodized Ta₂O₅ dielectric formation. The result is unmatched CV/g (capacitance × voltage per gram) and self-healing reliability which are capabilities few substitutes match without performance or size penalties.

Yet challenges abound: Global mine production (~2,500 tonnes of tantalum content annually) is heavily concentrated, with the Democratic Republic of Congo accounting for over half (~1,300 t), much of it artisanal/small-scale, alongside significant output from Rwanda and others /Stanford Advanced Materials/. Australia holds the largest identified resources followed by Brazil and others (e.g., the Greenbushes and Wodgina deposits in Australia, and the Mibra mine in Brazil). However, due to lower operating costs and higher-grade surface deposits, actual raw ore extraction remains concentrated in the Great Lakes region of Africa. End-of-life recycling from electronics remains very low (tantalum reports to copper smelter slags), though internal manufacturing scrap recycling is high and leaders like Global Advanced Metals push 100% recycled certified products.

Key players include integrated supplier Global Advanced Metals (GAM) for upstream powder, and an oligopoly of capacitor makers, KEMET (Yageo), AVX /YouTube/, Vishay, and Panasonic, controlling the vast majority of finished Ta caps. Niobium (or Niobium Oxide) capacitors offer a close alternative using Nb₂O₅ dielectric with supply advantages and safer failure modes. China, via companies like Ningxia Orient Tantalum, features in some processing/import streams, amplifying concentration risks amid AI-driven demand spikes that have boosted US apparent consumption dramatically to ~890 tonnes in 2025. In practice, engineers often mix technologies like multi-layer ceramic capacitors (MLCCs) with polymer aluminum or niobium for cost-optimized designs, retaining tantalum only where its unique combination of metrics is essential.

Looking ahead, as AI data center capex explodes, expect accelerated investment in capacity expansion, advanced recycling technologies, and supply chain diversification to mitigate bottlenecks. Tantalum’s unique capabilities make it indispensable for reliable, high-performance AI systems; securing ethical, resilient supply is foundational to the AI future.

Key Insights

How many tantalum capacitors are typically used in a high-power AI GPU server and rack?

Roughly 20 to 100+ ultra-low ESR tantalum polymer capacitors are utilized per high-power GPU accelerator board to supply localized bulk energy. With four GPUs plus intensive CPU power distribution networks per tray, a single compute node can harbor 100 to 400+ bulk capacitors, leading to approximately 1,800 to 7,200 tantalum capacitors in a state-of-the-art 18-tray AI data center rack.

Where does the raw material for tantalum capacitors originate, and what are the supply risks?

Over half of the global mine production of tantalum, which totals around 2,500 tonnes annually, is concentrated in the Democratic Republic of Congo. Due to the high concentration of extraction in the African Great Lakes region and the reliance on artisanal mining, the tantalum supply chain faces significant ethical, regulatory, and geopolitical risks that can disrupt component manufacturing.

What materials can engineers use as alternatives to tantalum capacitors in AI servers?

Niobium or niobium oxide capacitors serve as close alternatives to tantalum capacitors, offering comparable performance with safer failure modes and more diversified supply chains. To mitigate cost and availability issues, design engineers also utilize multi-layer ceramic capacitors (MLCCs) and polymer aluminum capacitors, reserving tantalum only where extreme performance is essential.