Hafnium High-k Dielectrics: Powering AI Chip Scaling Amid Supply Chain Risks

- David Rogers

- AI Buildout Supply Chain

- 2026-06-23

NEED TO KNOW

- Essential Gate Dielectric: Hafnium dioxide (HfO₂, k ≈ 25) replaced SiO₂ to enable sub-5nm, 3nm, 2nm, and GAA transistor scaling by slashing gate leakage current while preserving capacitance.

- Inelastic Byproduct Supply: Hafnium is recovered solely as a ~50:1 byproduct of zirconium refining, capping global primary output at just ~70–75 tonnes annually.

- Downstream Chokepoint: Downstream Zr-Hf separation capacity is heavily concentrated in China, creating geopolitical risk for precursor suppliers feeding TSMC, Intel, and Samsung.

- Domestic Supply Initiatives: Western diversification efforts include projects like IperionX’s Titan heavy mineral sands project in Tennessee to establish non-Chinese zircon and hafnium feeds.

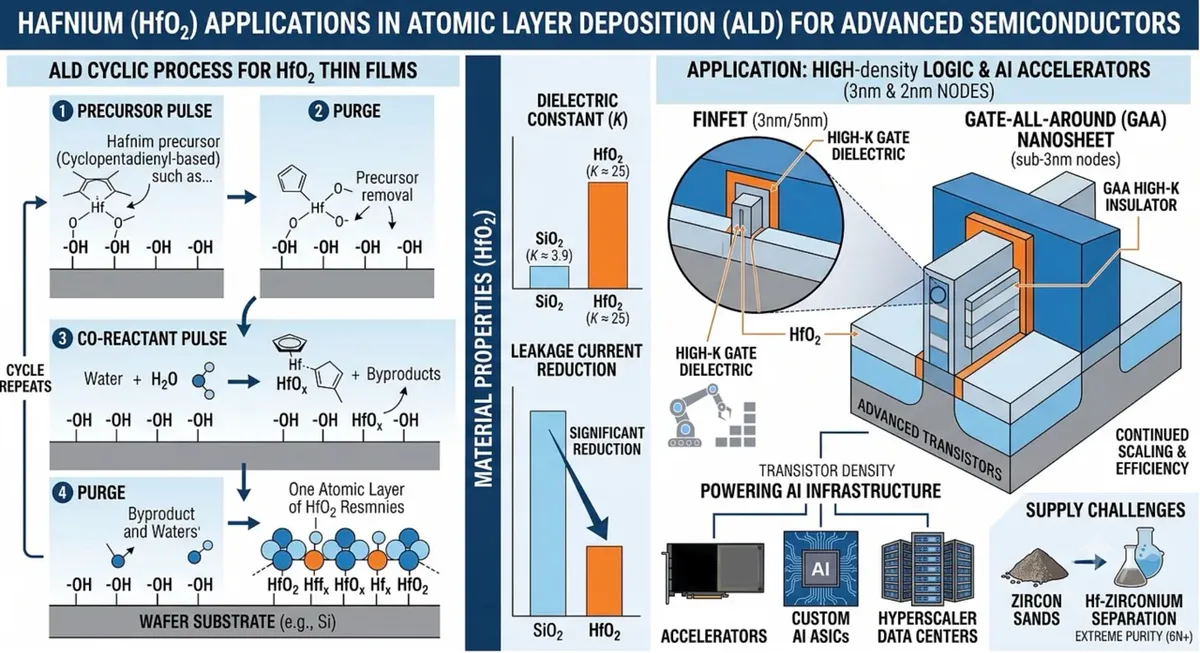

Hafnium dioxide (HfO₂) replaced silicon dioxide as the gate dielectric in leading-edge logic chips starting with Intel’s 45 nm node in 2007 /Intel/. Its high dielectric constant (~25 vs. ~3.9 for SiO₂) allows thinner effective oxide thickness, slashing leakage while preserving capacitance which is essential for continued scaling to today’s 3 nm, 2 nm (e.g., TSMC N2), and upcoming GAA/CFET nodes powering NVIDIA, AMD, custom AI ASICs, and hyperscaler accelerators.

Hafnium is extracted as a byproduct of zirconium refining from zircon (ZrSiO₄) sands. The Zr:Hf ratio is typically ~50:1 /USGS/, and chemical similarity (lanthanide contraction) makes separation extraordinarily difficult and costly. Industrial processes rely on multi-stage solvent extraction (e.g., MIBK-HSCN /MDPI/ or TBP systems /ScienceDirect/), ion exchange, or molten-salt distillation, followed by conversion to ultra-high-purity precursors such as HfCl₄ or cyclopentadienyl-based organometallics for atomic layer deposition (ALD) /ACS/. Semiconductor-grade material demands extreme purity with Zr impurities often <10–100 ppm and overall 6N+ levels to avoid threshold voltage shifts and mobility degradation in transistors.

Supply is critically constrained because hafnium is recovered only as a low-volume byproduct during zirconium refining of zircon sands bounded globally by nuclear-grade zirconium production. Major upstream producers — Iluka Resources (Australia’s leader with Jacinth-Ambrosia and the ramping Balranald project), Tronox, Rio Tinto’s Richards Bay Minerals (South Africa), and Kenmare Resources (Mozambique’s Moma mine) — mine and initially process the sands into heavy mineral concentrate and zircon via wet and dry separation. Global zircon output is roughly 1–1.2 million tonnes annually, mostly from Australia and Africa. China has rapidly expanded downstream zirconium-hafnium separation capacity through firms such as CNNC Jinghuan, Nanjing Youtian/Jiangsu Yichu (major new facility), State Nuclear Baoti, and Guangdong Orient Zirconic, now handling a large share of global refining and producing hafnium metal, oxide, and tetrachloride. Primary hafnium output is limited to ~70–75 tonnes per year, with recycling minimal and semiconductor thin-film recovery nascent.

AI-driven demand for advanced logic is the fastest-growing segment. High-k HfO₂ (and HfZrO variants) underpins the transistor density and power efficiency required for next-generation AI training and inference silicon. Overall hafnium market growth is projected at 6–9% CAGR through the early 2030s /Mordor Intelligence/, with semiconductor/AI infrastructure contributing meaningfully to the widening supply-demand gap and recent price spikes (unwrought Hf reaching multi-thousand USD/kg levels).

Geopolitical concentration risks are acute: processing capacity is dominated by a handful of players in France, the US, China, and Russia, with China-linked export controls on dual-use materials already tightening flows. Long-term supply security for AI chipmakers (TSMC, Intel, Samsung and their precursor suppliers like Air Liquide and Merck) depends on successful diversification—new mines, advanced separation tech to cut waste/cost, and higher recycling rates. Promising U.S. examples include IperionX’s Titan project in Tennessee /IperionX/, a fully permitted heavy mineral sands development with a completed DFS showing strong economics (after-tax NPV₈ of US$813 million, 39% IRR) and significant government funding support; it is expected to deliver meaningful domestic zircon concentrate production alongside titanium minerals and heavy rare earths. Without accelerated investment across such projects, hafnium bottlenecks could constrain the very compute scaling that AI buildout demands.

Key Insights

Why is hafnium critical for advanced AI microchips?

Hafnium dioxide is the essential high-k gate dielectric that enables transistor scaling down to 3 nanometer, 2 nanometer, and next-generation gate-all-around nodes. Its high dielectric constant of approximately 25 slashes leakage current while maintaining high capacitance, which is necessary for the performance and energy efficiency of logic chips powering AI accelerators.

What are the main constraints in the global hafnium supply chain?

Hafnium is a low-volume byproduct of zirconium refining from zircon sands, which makes its primary output strictly bounded by nuclear-grade zirconium production. Global primary hafnium production is limited to just 70 to 75 tonnes per year, and downstream zirconium-hafnium separation capacity is heavily concentrated in China, creating high geopolitical supply risks for advanced semiconductor manufacturers.

What initiatives are helping secure domestic hafnium supplies in the United States?

The Titan project in Tennessee, developed by IperionX, is a fully permitted heavy mineral sands project designed to establish a domestic supply of zircon concentrate, titanium minerals, and heavy rare earth elements. Backed by government funding support, this project aims to diversify the semiconductor supply chain by providing a non-Chinese source of raw materials for hafnium extraction.