The Germanium Chokepoint Powering AI Data Center Fiber and High-Speed Chips

- David Rogers

- AI Buildout Supply Chain

- 2026-06-22

NEED TO KNOW

- Optical Fiber & SiGe Backbone: Germanium dioxide/tetrachloride (GeO₂/GeCl₄) is the essential refractive index dopant in optical fiber cores and SiGe transistors, enabling multi-terabit optical interconnects across GPU clusters.

- Extreme Supply Concentration: China controls ~60% of refined germanium output through producers like Yunnan Chihong and China Germanium, leaving Western supply reliant on Umicore (Belgium) and Teck Resources (Canada).

- Surging AI Fiber Demand: GPU racks demand up to 36× more fiber than CPU setups, driving a projected 37% increase in global germanium consumption by 2033.

- Mitigation & Alternatives: Domestic substitution (e.g., LightPath's BlackDiamond chalcogenide glass) and expanded recycling of zinc residues/copper-cobalt cake are critical to lowering supply risk.

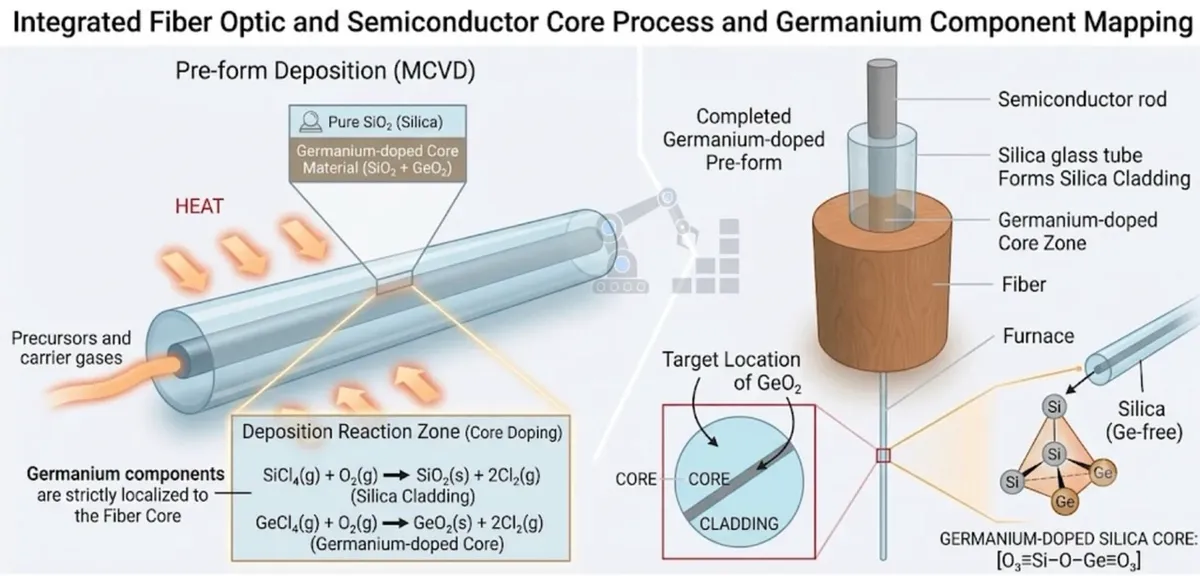

Germanium is the essential dopant in optical fiber cores and a key enabler in compound semiconductors and photonics. In fiber production, germanium dioxide or tetrachloride raises the refractive index of silica to guide light with minimal loss over long distances, a capability vital for the terabit-per-second interconnects linking thousands of GPUs in modern AI clusters. It also supports high-electron-mobility materials in high-speed transistors and infrared detectors. As hyperscalers pour hundreds of billions into AI infrastructure, germanium’s role in both massive fiber deployments and specialized photonic components has elevated it from a niche byproduct to a strategic chokepoint.

Production remains tightly concentrated and technically demanding. Germanium is recovered almost exclusively as a byproduct of zinc refining or from coal fly ash /MDPI/, with China controlling roughly 60% of global refined output through major integrated producers such as Yunnan Chihong Zinc & Germanium, Yunnan Lincang Xinyuan Germanium Industry, and China Germanium Co. The refining route involves hydrometallurgical leaching of residues, solvent extraction or precipitation to yield GeO₂ or GeCl₄ intermediates, followed by distillation and multi-stage zone refining to achieve the ultra-high purity required for fiber dopants and semiconductor-grade material /Springer/. Emerging secondary sources are gaining attention, including copper-cobalt cake generated during zinc electrolyte purification /Drzazga et al 2024 J. Phys.: Conf. Ser. 2738 012021/ , which contains recoverable germanium along with copper, cobalt, cadmium, and other metals. Recent research has demonstrated viable leaching routes to extract germanium from this cake, offering a pathway to increase supply from existing industrial residues. This complexity, combined with low ore concentrations and environmental management of acidic wastes, keeps primary capacity limited and slow to expand outside China.

AI-driven demand is accelerating sharply. A single modern GPU rack can require up to 36 times more fiber than traditional CPU setups /Tom’s Hardware/, driving projections that the U.S. alone will need 213 million additional fiber miles by 2029, more than doubling the existing installed base. Fiber optics already account for about 30% of global germanium consumption (with broader telecom and infrared optics exceeding 50%), and AI-specific needs are expected to lift overall demand by around 37% by 2033. Additional growth is coming from germanium’s use in high-speed SiGe transistors, photonic integrated circuits, and specialized detectors that support optical I/O and co-packaged optics in next-generation AI systems.

Geopolitical and supply-chain risks are acute. China’s export licensing regime and past restrictions have already caused sharp price spikes, germanium metal prices have more than doubled between early 2024 and early 2026, while Western import reliance remains high. Key non-Chinese upstream players include Umicore in Belgium (the leading Western recycler and high-purity GeCl₄ supplier) and Teck Resources in Canada (byproduct recovery from zinc). Downstream, LightPath Technologies (LPTH:NASDAQ) offers a notable U.S. response in the infrared optics segment /LightPath/. The company has developed proprietary BlackDiamond™ chalcogenide glass as a domestic alternative to germanium lenses for thermal imaging and IR systems. Vertically integrated from raw glass production in Orlando to coated assemblies and EdgeIR™ AI-ready cameras for industrial monitoring and defense applications, LightPath is reducing reliance on Chinese germanium while aligning with NDAA and DoD priorities for secure supply chains. These players are expanding recycling and processing, yet meaningful new primary capacity outside China will take years to scale.

The path forward hinges on aggressive recycling and Western diversification, with secondary sources like copper-cobalt cake from zinc refining representing a promising near-term opportunity. Umicore already sources more than 50% of its germanium from secondary streams, and 2024 research on leaching germanium from copper-cobalt cake demonstrates practical routes to unlock additional supply from existing industrial residues. LightPath’s domestic BlackDiamond production and germanium-free camera variants further illustrate how U.S. firms are commercializing substitutes. While recovering germanium from deployed fiber remains technically challenging, policy support through the U.S. Defense Production Act /Breaking Defense/ and EU Critical Raw Materials Act is funding domestic refining and recycling projects. Innovation in residue processing, improved purification yields, and strategic offtake agreements will be essential to prevent bottlenecks from slowing the AI buildout. Germanium illustrates how tiny volumes of specialized materials can create outsized strategic vulnerabilities, and why building resilient, circular supply chains is now a core priority for the AI era.

Key Insights

What is the primary role of germanium in AI data center infrastructure?

Germanium is the essential dopant in optical fiber cores and is critical for high-speed silicon-germanium (SiGe) transistors used in transceivers and SerDes. In optical fibers, germanium raises the refractive index of silica to guide light with minimal loss over long distances, enabling the high-bandwidth, terabit-per-second interconnects that link thousands of GPUs in modern AI compute clusters.

How is germanium produced, and where is the supply chain concentrated?

Germanium is recovered as a byproduct of zinc refining or from coal fly ash, with China controlling roughly 60% of global refined output. Key Chinese producers include Yunnan Chihong, Yunnan Lincang Xinyuan, and China Germanium. Outside China, major processing and recycling are led by Umicore in Belgium, while Teck Resources in Canada recovers germanium during zinc refining.

What alternatives exist to mitigate supply chain risks associated with germanium?

Chalcogenide glass, such as LightPath Technologies’ proprietary BlackDiamond glass, serves as a domestic alternative to germanium for thermal imaging and infrared optics. Additionally, processing secondary sources like copper-cobalt cake from zinc refining and expanding Western recycling capacity, such as Umicore's secondary streams, are key pathways to reducing dependence on primary Chinese germanium.